The top 1 per cent of Americans now own a staggering 40 per cent of the country’s $54 trillion of wealth. This is an extraordinary figure. When taken together with the fact that wages as a proportion of national income have been falling in the US since the 1980s, we see a vision of a society where the average person’s income is faltering, yet the wealth of the super-rich has never been more extreme. As a result of the fall in the share of output represented by wages, the share represented by profits has gone up sharply, and corporate America is now sitting on more cash than ever before.

This can’t continue. The pendulum will move back in favour of the average worker. The only questions are how . . . and when? Will it be gradual or sudden? Remember, the last time we saw such disparities between the hyper-rich and the average guy was at the beginning of the Great Depression.

The following three decades saw policies introduced by Washington to narrow this gap, ushering in a period of the American Renaissance during which levels of education and opportunity for all increased dramatically. This was truly the era of the American Dream.

The American Dream is now broken, but the aspiration is not extinguished. It is this aspiration that will be the driving force behind the move to narrow the gap between the super-rich and the average.

The re-emergence of the ordinary Joe is not just a political question; it is a question of economic survival, too. After all, where does corporate America think consumer demand comes from? It comes from the income of the average guy – and wages are his income.

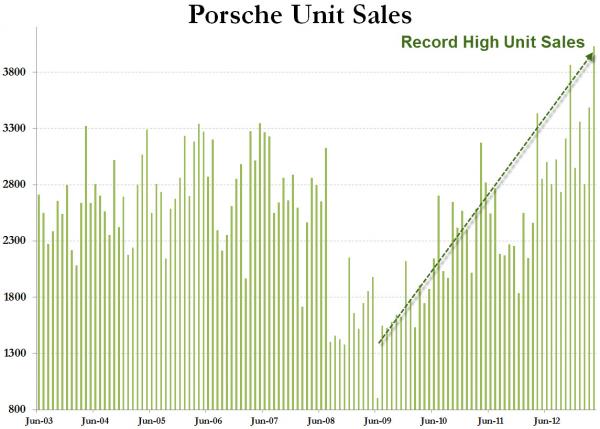

At the moment, high-end goods are selling well in the US. Look at the chart for Porsche sales above. They are booming. Who is buying these Boxsters and Cayennes? It’s certainly not the average dude. Yet it is the average dude that Ben Bernanke is hoping to help by his policy of printing money. Bernanke is on record as saying he wants to drive up stock prices, to create a wealth effect for Americans, making them feel wealthy, coaxing them to spend and, in so doing, kick-starting the economy.

It is against the background of income disparities that I would like to look at the present policy of the world’s central banks.

The policy of printing money and pumping up the stock market has two very serious dangers for the rich all over the western world, but in America in particular.

First, the policy is making the rich very much richer because they own the assets that are rising in value and more and more money is pumped into the financial markets. This obviously exacerbates the gap between rich and poor. It also greatly increases the risk of a market crash because, if the only thing keeping stockmarkets at historically high levels is cheap money, then how do the central banks turn off the taps without precipitating a crash?

The second dilemma for the rich is that, as the gap widens between them and the rest of humanity, the natural human craving for fairness and having a slice of the pie will mean that, if the system crashes, the appetite for political forgiveness could be finite.

The first dilemma is something that is perplexing many investors.

We know that printing money by the trillions of dollars raises the prices of stocks and bonds. This forces down the rate of interest, which slashes the cost of servicing government debt. So all looks OK. But it’s hard to imagine the slowing or stopping of quantitative easing (QE) without major adverse effects on the prices of stocks and bonds and the performance of the economy.

But what if only the super-rich benefit and the average Joe is terrorised by rapacious management at home and globalisation abroad, both forcing down his wage?

In such circumstances, the economy doesn’t recover because the income of the regular dude remains suppressed. Then, as the famous investor Paul Singer said last week, “the exit from QE is somewhere on the continuum between problematic and impossible”.

The central banks of the world are then caught in a classic catch-22 situation. They can’t stop printing money because this would cause the whole deck of cards to come crashing down; they can’t keep printing money because this only creates the conditions of an even bigger stock and assets price crash.

The problem is that, at current growth rates, the world economy is far too weak to support current asset prices without more central bank credit easing. Unless that changes, an attempted exit would cause a massive correction in risk assets.

Such a crash would mean a return to depression-like economic conditions. The alternative is, of course, to keep printing irrespective of inflationary consequence, maybe leading to stagflation – a situation where inflation rises and output falls.

The problem now for the global markets is a bit like the problem in the Irish housing market when we were getting close to the top. Most analysis suggests that the credit explosion is driving the rise in prices, but what if it’s the other way around?

What if the rise in stock prices is driving the lending? At the top of the boom in Ireland, the rise in houses prices prompted further lending, because the rise in prices validated the next bout of reckless lending.

The balance sheet began playing tricks on both lender and borrower. As asset prices rose, imprudence began to look like prudence, recklessness like sanity. As house prices rose, more and more ‘equity’ was released, pushing prices yet higher.

Given these risks, you would imagine that the central bankers might sound a bit worried about everything. But every time I listen to Draghi et al, all I hear is swaggering masters of the monetary universe. Maybe they know where all this is leading, but calamity in a few years becomes a secondary consideration when compared with the desire to avoid immediate pain and, most of all, blame.

All the while, for the super-rich, the chance of a gradual, gentle pendulum swing back to the average guy diminishes – and something much more violent becomes possible.

Subscribe to receive my news and articles direct to your inbox

Does this mean I am first?

U2 Poverty is not fate .It is a condition ; it is not a misfortune , it is an injustice .It is the result of social structures and mental and cultural categories , it is linked to the way in which society has been built , in its various manifestations. The Christian engagement with the poor is not a choice , it is an obligation .The Christian is not called to share what is left over but rather to share equally , treating other humans with respect . Above all , it means channelling energies and talents on behalf of… Read more »

David: “The top 1 per cent of Americans now own a staggering 40 per cent of the country’s $54 trillion of wealth” and “As a result of the fall in the share of output represented by wages, the share represented by profits has gone up sharply, and corporate America is now sitting on more cash than ever before.” I am not disputing your figures but I would like to know exactly where this oft-quoted “1% of Americans own 40% of U.S. $54 trillion wealth” comes from. Are these individual Americans or are some of them corporations because under U.S. law… Read more »

Your starting to deliver a more complete analysis now David, fair play.

…. typing to quick should have been……. You’re

Just a few facts to digest: – Debt growth in emerging markets is still at an anual growth rate of 20%. Source: Allianz Global Wealth Report 2012 ! – More than 80 percent of the world’s population lives in countries where income differentials are widening. Source: HDR / Human Development Report 2007 – In 2005, the wealthiest 20% of the world accounted for 76.6% of total private consumption. The poorest fifth just 1.5%. Source: World bank developing indicators 2008 – For every $1 in aid a developing country receives, over $25 is spent on debt repayment. Source: World bank data.… Read more »

In addition to my post above:

In 2011 total development aid was the equivalent to 0.31% of developed-country combined national income USD or 133 bn.

The commitment was USD 300 bn, or 0,7% of combined national income.

Source: UN integrated implementation framework

As for the larouchepac indoctrination of this blog:

I pointed that out to David and others more than a year ago.

My suggestion from back then:

Sticking to free speech, but enable the blog with a IGNORE function. So the use who does not wish to be bombarded with the same old same old political right wing cult pestilence has a choice. By pushing this button, all conversations coming from BonBon are hidden, including those messages who still are feeding this troll by engaging with him.

Would give th blog slim feet. LOL

David, thanks for speaking out me.

Regards,

Joe

The fear of failure and political reality the politicians can’t tell the plebs the world is going to end as that would self fulfilling.

So does this mean you are on the way to concluding that the money system as is is broken – a revolution may be the best we can hope for? A patch up job may be a disaster.

There is something deeply dysfunctional at the heart of the economic structure of the US economy. The media representation of the debate about income distribution, is itself extremely compromised, and patronizing. It is actually designed to operate a status quo of two very narrowly defined, superficially opposed, but realistically equivalent options. America, under the policies of Greenspan/Bernanke, and under the cultural ethos of the Show Business sector (which is the dominant cultural force in the US, and has no competitors), has seen an accentuation of movement at the extremes. The rich get richer, and the poor borrow more. Obama sold… Read more »

There is a massive disconnect, even in this country, between the value if the ISEQ index, and the real situation that people experience every day. And this is in a country with a massive capital shortfall, and massive debt repayments. [ “we all partied” – now the hangover]. The key driver of much of this is ECB interest rate policy. Once they made the mistake of setting rates too long, for too long in the first place, it was only a matter of time before they would end up setting them too low forever. We are heading for a market… Read more »

I believe we are past the point where, even if we are to accept that “we all partied”, we have now paid the piper, seems to me the bankers and politicians are still partying while joe soap is penalised more and more in order to prop up the party, enough is enough…my biggest fear is my worst fear, that this will all end in war, for with the weapons now available to all sides, the outcome is truly terrifying regardless of who wins.

David, word by word, your explanation is excellent, and could be understood perfectly all right, by the citizens of any country, with a general interest in current economic and political affairs. . And also I find Deco’s commentary superb! . Do you think that people associated to power, and behind big corporations, who allowed the system to be so evil, is going to change overnight, for the sake of humanity or society? Think again David! . When the political establishment in Switzerland, backed by big pharma companies, wanted to exclude alternative methods of medicine from the national health system, the… Read more »

So quackery is the order of the day in Switzerland is it?

Said Quackery didn’t serve Steve Jobs very well.

I’m all for new therapies but they have to be solidly evidence based.

I´d say printing money is actually damaging the rich in order to save the debtors. But as the debtors mostly owe their debt to the rich anyway its a convenient temporary arrangement. As soon as the rich decide their debt slaves are back on an even payment keel theyll end the money printing and raise interest rates. In Ireland the tracker mortgages symbolise the rich persons dilemma…

Even with all the inequalities in the american system, it is still 100 times fairer than the european systems of 18th and 19th century. You only have to look at how the british empire was run to see that, only the elites and the toffs in that system could hold property and wealth and if you were the wrong religion forget it. At least in the american system anyone can attain wealth, and anyone can buy shares in the corporations that are making the profits. I know the stock market has alot of faults that work against the ordinary joe,… Read more »

The Incas and other cultures from South America knew how to use certain plants for contraception, and some people still use it today. They know what herbs to use to dissolve stones in your kidneys, and in Paraguay some people know what type of plants can be use to treat people with tumours. I have an Irish friend that had a tumour in her thyroid gland, and modern medicine here wanted to remove it from her body. She refused it and took control of her own cure, through detox, diet, and herbal infusions. I saw the lump of the size… Read more »

Going back to the main topic of discussion there is an excellent book titled Third World America written by Arianna Huffington subtitled How our politicians are abandoning the ordinary citizen of which Joseph Stiglitz said “It is an alarming account”.

It all looks rather overwhelming. Armageddon like even. Early 20th Century 1st 20 years …arrival of Flight, 1st World War and demolition of a major Monarchy and then a market crash. We then moved on. Whether we like it or not, we work according to a plan. Seeing lives of few people destroyed in Boston during a marathon – that’s NOT our plan. Seeing a building collapse and kill off 1000 workers, we still keep buying cheap garments – that’s IS our plan. The plan is about day to day security of mind, the same one that allows you travel… Read more »

Greed greed and more greed. The great Depression there will always be winners and losers as far as the rich are concerned. How to stop the poor getting poorer. For a lot of people everyday is a struggle,people need to realise its us verses them . It use to be us and them,living here as far as I can see there is the majority of people being talk down to and being told to live on less,from a government that lives on more. This government want judges to take less hoildays on one hand but don’t say anything about there… Read more »

DMcW is spreading fear and loathing. It sells obviously. Now he is promoting violence, sorry “describers” a pendulum swinging. Or was the ballistic flight of the guillotine?

Say it ain’t so DMcW!

Maybe DMcW wants a place on the Committee of 10?

Instead reject that “description” your finance mates are frothing. Stand out, possibly on your own”, take the flak, and promote the only thing that can work.

We are greater than our statistical destiny.

Otherwise chimps would be blogging here.

An alternative to the guillotine, that particularly European “solution”, is an American idea, and DMcW chose the US as his theme, from a West Brit point of view.

Contrast the induced European haplessness to this :

Summary of State-Level Activity in the National Glass-Steagall Week of Action

Now Ireland does look more to the US more than London, whatever West Brits think. DMcW has no choice but to deal with this one way or the other.

Interesting some brought up “homeopathy”. Actually it was bound to happen. The long “descriptions” of statistical “facts” being trotted out here mean the medicine is diluted to almost non-existence. And then presto, magic- it is supposed to work more effectively! We have here in fact a homeopathic blog! The founder of Homeopathy, Hahnemann, wrote it was based on the idolized Kant : the unknowability “in itself” of the disease meant to combat it with medicinal action that is unknowable “in itself” also – hence dilution. Kant is required study for all homeopathic’ers. That kind of “medicine” the rats, bugs, and… Read more »

The Irish have ghost estates, the Spanish have ghost resorts, the Americans have ghost commercial parks, the Chinese have ghost cities, as ultimately the world has a ghost economy. Milton Friedman on a junket to China noticed canal diggers using shovels, questioning the bureaucrat why they were not using machinery the bureaucrat replied “to create jobs”. “Well if that’s the true purpose of the project then simply give them spoons and you will create far more jobs.” The world economy is increasingly spoon-driven as the wealth-generating jobs are automated/mechanised/digitised and the surplus labour becomes the majority, the opposite of a… Read more »

Some might enjoy this:

http://www.thebaffler.com/past/practical_utopians_guide

Is Merkel a fraud ? http://mobile.reuters.com/article/idUSBRE94C0LZ20130513?irpc=932 It is like as if she is just a careerist chasing power, irespective of ideology. A bit like the rest of the EU leadership. Something has gone very wrong with the whole project. The obsession with control and power is now the over-riding objective. If the people are not obedient, then they get a technocrat government. Maybe there is a file on her in Moscow, praising her enthusiasm for Marxism. Because, currently she is a fan of the market. After the Cyprus debacle, a picture mysteriously emerged, on the internet, of a younger Merkel… Read more »

Pop quiz below after an excellent article David. We spoke about the ‘printing of money’ before. I was arguing that it’s very misleading because it gives the impression that the central bank creates all the money in the economy for the Government. Most people think we have ‘everlasting money’ from this also. As you know only 3% of euros/dollars exists as cash. The other 97% is electronic money and exists as our bank balances. This money is created by the commercial banks through loans and I think this is a huge factor in analysing the debt crisis. You were saying… Read more »

An interesting view of Ireland, Spain, and the rest

http://theautomaticearth.com/Finance/if-the-rest-are-only-half-as-bad-as-ireland.html

Ahhhh America..home of the free,Land of the WATCH OUT ITS BEHIND YOU! brave The shining city on the hill….BOO ! The peace loving Country that brought us such hits as Vietnam, Panama, Grenada,The “Mog” [Somalia] Gulf War 1, Gulf War 11 Afghanistan,Yemen,Pakistan The Drone Brothers,Guantanamo,illegal rendition..C.I.A N.S.A HOMELAND SECURITY..THE PATRIOT ACT..N.A.D.A F.B.I. A.T.F….for your protection…….. Lets not forget the old classics….Lebanon , Chile , Ecuador , Niagara , Laos , Cambodia, Bosnia ……and all the wonderful democratically ELECTED GOVERNMENTS [52] they overthrew………. 32 Countries attacked since 1947 and still growing…. America…the Country that brought us the first Genocide…. 100 million… Read more »

Does revolution work? We can never know the answer to that – we may still be living in monarchic societies if not for the revolutions of the past, maybe even worse – freedom is not free – we are in this mess because the masses are not involved in there societies they live with wishful hopes and expect others to do right by the masses the masses defer to groupthink. The system is broke and those in charge of it have signed up to preserve it (their egos partly rule) even if they wanted to they cannot tell the truth… Read more »

A revolution is necessary Joe. But in today’s World.. everyone who thinks outside the box..is a subversive or a Terrorist or anti-establishment or some other label. Everyone has to be labelled or bar-coded or have to fit in some demographic. For a Society to survive , one needs to create a evil , a monster for the masses to be afraid…control the masses ,control everything else..anybody who does their own thinking.their own research..is challenged, ridiculed,laughed at.. demonized as a quake,a conspiracy theorist. The American War on Terror is a brilliant plan..never ends..no borders..no Country and if you don’t toe the… Read more »

“Brush aside talk of bubbles and get back to work”

http://www.irishtimes.com/business/economy/world/brush-aside-talk-of-bubbles-and-get-back-to-work-1.1391894?page=2

Guys Those of you contemplating revolution better move fast…you WILL comply. Pain ray: The US military’s new agony beam weapon 16 May 2013 by David Hambling Magazine issue 2916. Subscribe and save For similar stories, visit the Weapons Technology Topic Guide THE pain, when it comes, is unbearable. At first it’s comparable to a hairdryer blast on the skin. But within a couple of seconds, most of the body surface feels roasted to an excruciating degree. Nobody has ever resisted it: the deep-rooted instinct to writhe and escape is too strong. The source of this pain is an entirely new… Read more »

something shitty goin on with AIB …more than usual…?

For Paul Ferguson

http://www.dailykos.com/story/2013/05/10/1199289/-Of-course-money-doesn-t-grow-on-trees-its-not-a-commodity#

While many here are grasping for violence, murder is being committed right now by the Troika. It is much better to stand for a principle, a true universal principle, taking the risk of a barrage of attacks, than to add to the bestiality. “The Body Economic:Why Austerity Kills” The New York Times today published an op-ed by two researchers from Oxford University and Stanford University who have published a book, due out May 21, documenting that the austerity policies of the IMF and the Troika kill. The authors of The Body Economic: Why Austerity Kills, summarized their findings today in… Read more »

The world is falling apart and the only priority news that I am getting is Angelina Jolie Boobs being shoved in My Face…

All this talk of revolution etc needs a little bit of grey matter and some matter of fact actions. I asked earlier that given what can we do about it? By that I mean what is now 100% within our remit to do NOW. Now some will yammer again about GS etc. But that’ll never happen because it will not be entertained. BUT!!! It or similar could indeed happen because of what people decide to do now. I met a few of the guys on this blog and without a scintilla of exaggeration, all are extraordinary individuals with deep talent… Read more »

Mysterious indeed. It’s snowing here at 800m in the pyrénées!

So for the francophiles among you, here is a very moving radio interview with Charles Palant, a French Sage indeed.

Born in Belleville, Paris in 1922, Jewish by religion, parents who had come from Poland.

This is the second part of the interview, which starts at 4 min.30sec.

http://www.la-bas.org/article.php3?id_article=2768

Can’t resist this:

http://www.nasa.gov/multimedia/videogallery/index.html?media_id=163003001

I cannot fathom why some insist that Noonan and the boys will not simply harvest the “low-hanging fruit” – your savings. The voracious appetite of the banking morass can only be cauterized, not appeased : Bail-In Bank Heist Coup D’etat May 14, 2013 (EIRNS)–“Bank resolution” for the imminent failure of the entire Eurozone’s banks was “debated” today, May 14, at the EU Finance Ministers’ meeting in Brussels. The debate focussed on what degree of bail-in could be agreed upon in the — to use bankers’ jargon — “recovery and resolution” of failing banks. This is the main pillar of a… Read more »

Glass-Steagall is a challenge to the littleness of some here, and there in the Dail, and really just about banking. It is about evolution of the us, the human species.

That imposed littleness leads to a statistical destiny, a favorite of West-Brit economists.

Is DMcW showing what will happen unless…?

Why not instead state the “unless”, not pass over something not to be talked about. What prevents free expression? That is tying the tongue or pen?

A friend of mine said he seen Ming in Dublin the other day driving and talking on his phone so no lesson there.

Wall Street Gurus Warn of Massive Collapse Underway

Is this report, from Mohamed El-Erian, CEO of PIMCO, the world’s largest bond fund whom DMcW mentioned a while back, the reason for the alarm?

Colin “Why didn’t people go fishing to survive?” Colin Are you a revisionist / apologist for genocide? Or are you Jesus? If so there are starving people though out the world that could use your services. Can you catch mackerel all year round from loop head or is just late august early September – difficult to feed 8.5 million people with some feathers and with only a few weeks of a fishing season unless of course you can turn water in to wine and such like. The British were exporting food from Ireland while Irish people were starving this was… Read more »

Joe, every newly elected prime minister, president, pope etc, usually starts off with a formal apology of some sorts for past actions by previous governments. This looks good and most likely there is a budget set aside for such an apology.

Any admissions occurring during the lifetime of a government is only done if and when the people involved have deceased or a handful is left. The timing is also carefully chosen.

Are you saying the famine did not happen too and that all people had to do was fish.

No,not all new PM make apologies-what ridiculous statement.that why Blair traveled the news media of the world.

One could argue he should not have since he was not a round.

the point is the famine happened and the british exporting food from people that were dying.

Making excuses for it does change those fact it does show the subservient mentality of some Irish people

{Fashionably late as usual}

David,

If my spending is your income, and your income is mine and I’m an average Joe and I have no spending, but owe the 1% a fortune I’ll never pay, not because I won’t but because I can’t, and the 1% get wealthier on central bank printing of money and not ‘stuff’ they provide or sell to me, cos I can’t afford it, then surely there will be no need for violence as nature takes it course.

“Wealth gap can’t keep growing”

Oh yes it can and is and it will, particularly in Ireland because we are so subservient now and politics is redundant.

Your only hope now, if your not already winning, is the Lotto. It’s sad but true.

http://m.youtube.com/watch?v=QPKKQnijnsM&desktop_uri=/watch?v%3DQPKKQnijnsM