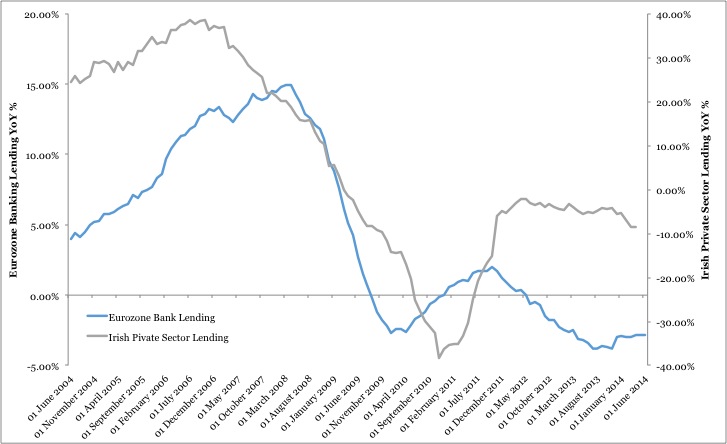

If you only have to look at one chart this week, let it be the one on this page (chart one).

It shows how Europe and Ireland have become cash economies because bank lending has collapsed. This slump in bank lending is why the European Central Bank (ECB) introduced revolutionary measures last Thursday. These new moves by the ECB may have a significant positive impact on our economy in the years ahead, because they will now reward banks that lend and penalise banks that don’t. Significantly, the ECB will not reward banks that lend to property. This is a crucial positive for Ireland.

Since the crash in 2007-2008, bank lending has fallen progressively everywhere. This is what always happens after an asset bubble. The people have too much debt and they don’t want to borrow and the banks have too much bad debt and they don’t want to lend.

In such an environment, even good projects can’t get financed and therefore this type of recession – one where there’s too much legacy debt – goes on for much longer than other recessions. Globally, since 1945 the average recession lasted 10 months, this one feels like it’s been going on for years.

One of the traditional roles a bank must play in an economy is that it must recycle money from savers to borrowers. There will always be people who want to save and there will always be people who want to invest. The bank should match these people together offering savers a place to put their money and offering investors that same money to invest.

But if banks are not lending, the savings, when they are put in the bank, stay in the bank and don’t get recycled out into the rest of the economy.

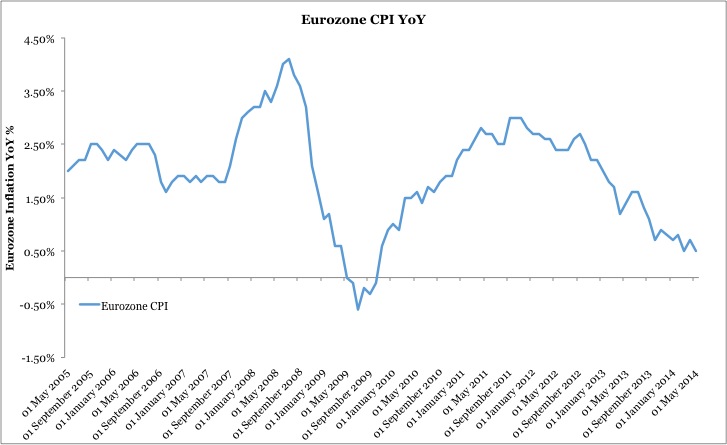

This bottleneck chokes off recovery and allows deflation to take hold. Deflation is when prices are falling. This process can become ingrained if after a few years of falling prices, people expect prices to fall, not rise in the future. (See chart two.) This is what happened in Japan from 1990-2010.

{kind=link}

Deflation is precisely what the ECB has now moved to fight. But it won’t be easy, because nobody is sure that the latest initiative will work. If it doesn’t work quickly, the ideological sceptics in Germany will force the ECB to abandon the experiment.

To see why the Germans are not behind ECB president Mario Draghi all you need to do is examine recent history. In fact, the D-Day celebrations this week are a good place to frame this history.

One of the interesting aspects of the defeat of the Nazis was the unbelievable success of the country that emerged from the ashes, namely West Germany. At the core of the Federal Republic was a constitution which protected the citizen’s liberty against the state and a powerful constitutional court in Karlsruhe to police the state on behalf of the citizen. The other institution was one that protected the citizen’s money against the State: the central bank – the Bundesbank in Frankfurt.

From day one, the aim of the Bundesbank was to protect the citizen’s savings from inflation, which had destroyed the German economy in the early 1920s.

When the problem is inflation, the solution is deflation.

Heresy

However, what the Bundesbank never contemplated was what happens if there is deflation. By logical extension, if the problem is deflation, the solution is inflation. But it is heresy for central bankers to embrace inflation – however, that’s what Draghi knows they have to do.

Writing as a former central banker, schooled in the traditional way to be always on the look out for inflation, I know how difficult it is for these guys in Frankfurt to accept that they have to turn policy on its head and generate inflation now.

To execute this new strategy, Draghi has presided over a very un-Germanic coup at the ECB, where the Germans have been out-gunned, out-thought and out-voted. To put it bluntly, last Thursday Draghi wrote the obituary for the Bundesbank. The ECB is deeply Latin now. And it is doing what all Latins do in a crisis: print money.

The ECB has pushed rates down towards zero and says rates will stay there for four years..

It has also unveiled a new LTRO scheme which is, in effect, a giant cash for trash scheme encouraging banks to lend to the real economy, all financed by a money printing central bank. The new scheme will allow banks to exchange dodgy assets on their balance sheets for real cash and the bank can then lend this real cash to companies. Crucially, the new scheme can only be availed of by banks that prove they are lending to the real economy. This is a new and significant development because it means that banks will be rewarded for lending to the private sector firms that need financing.

This plan gives banks time to plan how they want to offer the money to the economy. It puts the ball firmly in their court. Let’s hope they do something this time. This is an intriguing development and it shows that Draghi is prepared to tear up the rulebook scripted by the German Bundesbank and replace it with his own new version to fit the new deflationary reality.

The impact could be most significant on the periphery where the credit crunch is most damaging. Tellingly for Ireland, he has stipulated that bank lending need to rise, but this rise can’t include property lending. This doesn’t mean that Irish bank will not lend against property (which is the risk), but that it will be more profitable for them to lend against other stuff.

If this re-balances Irish bank lending away from property into start-ups and companies which produce things, it could be a huge positive for an economy like ours that has a weakness for destroying itself with its property obsession.

At this stage, it’s a big if. But we have to give it the benefit of the doubt. At least after seven years of fighting deflation pressures with more deflationary pressures, the ECB has admitted that it was wrong all along. The solution to deflation is inflation and, God knows, Europe could do with a bit of that right now.

David McWilliams hosts the Dalkey Book Festival June 19-22nd. dalkeybookfestival.org

Morning.

“One of the traditional roles a bank must play in an economy is that it must recycle money from savers to borrowers. ” While we persist with that myth we’ll get nowhere. Banks do no such thing. What they do is recycle borrowing into saving. The borrowing (balance sheet expansion) always comes first. When banks balance sheets are contracting (borrowing shrinking) then we get a shrinkage in circulation *and* saving. Banks will only lend to creditworthy borrowers prepared to pay the current cost of money. That is always the limiting factor. Unless you are prepared to underwrite people who are… Read more »

Meek Inherit the Earth

Unlike the M25 ( London ) and Le Periferique ( Paris ) where what goes round comes round the M50 ( Ireland ) just does not go round ….it drowns .And when it goes Under …then it stays Under ….and when it stays under …it Never comes up .Because there is Nothing there .

Some of the earliest mammals that decided to arrive on land and initially had webbed feet .

It is time for Irish Borrowers to put back on their webbed feet and learn to swim again .

David, you should get a permanent gig on the Radio airwaves.

I suppose if you subscribe to the neo-liberal view of economics then it the ECB becomes a one trick pony,i.e. adjusting base interest rates.

Of course they do cloak their “interest rate adjustment” pronouncements with all sorts of mumbo jumbo bolloxology best decyphhered by their attentive and deferential Dept.of Finance guru’s/ boffins throughout the EU. yawn yawn yawn

“This is a new and significant development …” Sorry, David, but you’re over-egging this. You should have included the before/after numbers. Draghi’s announcement on Thursday dropped the lending rate from 0.25% to 0.15% and dropped the deposit rate from 0.0% to a negative -0.1%. A miniscule change. Besides, negative deposit rates have already been tried and tested to no avail in Denmark and Sweden. Likewise Draghi’s new LTRO scheme of e400b of cheap credit for banks to lend to SME’s (again tried and tested to no avail in UK and Netherlands) has also proved ineffective in an environment of saturated… Read more »

Where exactly is this deflation we keep hearing about. Food prices are rising at well over 10% per annum and that is global. Car tax, house insurance, public transport and most other essentials are rising. We even have the much heralded rise in house prices which has the property porn guys getting themselves into a right twist. The only area where there is and has been consistent price deflation is the phone and tech gadget market and prices have been dropping in this segment for over ten years with actual increased demand so price deflation has NOT postponed spending in… Read more »

From Mises, “Planning for freedom” 1952, talking about the post Malthus-Say debates of the early 1800’s. “Those authors and politicians who made the alleged scarcity of money responsible for all ills and advocated inflation as the panacea were no longer considered economist but “monetary cranks”. The struggle between the champions of sound money and the inflationist went on for many decades. But it was no longer considered a controversy between various schools of economist. It was viewed as a conflict between economist and anti-economist, between reasonable men and ignorant zealots.” Welcome to the world of monetary cranks and ignorant zealots… Read more »

If Ireland’s cost of living index was on a par with other countries, then maybe you could argue that we need inflation (although I cannot see myself agreeing with this argument)

But our cost of living index isn’t low, so how is inflation going to help us.

Excellent point made by whoever mentioned the tech industries and how lowering prices has only helped those industries.

Talking of inflation and deflation in relative terms and deficits and suplusses,and these articles, there is the following observation. A while back it was not unusual to get 200 comments and even 300 plus from time to time. Management considered this a surplus and took auterity measures and cut many contributions. The result has been that over the last months there has been a deficit of comments in numbers as often the contributers were reduced to less than 50. It is questionable that the quality of the content diminished as well. Many times the comments have disagreed with the premices… Read more »

It is the key idea of this economic argument ,and I’ve never seen anyone try and dig into it: ‘deflation causes people to wait before buying things because they know the price is going to fall’. There are some things it clearly isn’t true for – food, energy, cars, tech kit, clothes, home furnishings, in fact everything. How do I know this? People will pay 30% a year so they can have it this month, rather than next. People will mortgage their homes (stripping the kids of inheritance) so they can have it now. People don’t wait, even if there… Read more »

nothing the banks or bankers do will repay the outstanding debts owed by so many they can no longer borrow free money and repay it.

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/6/9_This_Will_Bring_The_Entire_Global_Ponzi_Scheme_To_Its_Knees.html

+1

We are living in a new era and the dead ordinary consumer’s attitudes and habits have changed dramatically. I see more and more young families trying to avoid buying a house in Ireland. They look at ways of staying in their parent’s house, rent a house or moving abroad. Buying a house is for many just a dream and/or a nightmare. A big change of sentiment from the good times. So I don’t see people spending that money that they have on the items that they used to spend their money on.

Have governments not inflate the housing bubbles by their own first time buyer’s schemes? Where did these subsidies go? To the young innocent buyer or to the developer? The developer of course – as the developer put that on top of the asking price. So, how can we inflate the economy this time?

Maybe we should all buy a good photocopier so that we can all simply photocopy our own money. Would save the government printing money.

“Governments would then be the very apparatus through which the bulk of the new money trickles into the economy — which also means a drastic expansion of government’s share in the economy at the expense of individual liberty.” Rather the look as last resort should be on the production of central bank money by all and any means possible. Within this attachment link will be found a discussion why governments will print and expand the money supply (inflation) at any suggestion of contraction and why it is not in our best interests to have that happen http://www.whatamimissinghere.com/archives/36396 It embellishes the… Read more »

“This slump in bank lending is why the European Central Bank (ECB) introduced revolutionary measures last Thursday. ” Those who did not borrow, but saved, during the central bank induced credit fueled boom are now in posession of cash and taking advantage of falling prices. Castigated as hoarders in previous lectures in the pages they are now stepping up and using their frugality for their own benefit. Those used to borrowing to live are out of credit and can afford to borrow no more. Therefore the contraction in borrowing is lightly the result of too much debt. This does not… Read more »

“Globally, since 1945 the average recession lasted 10 months, this one feels like it’s been going on for years.” It has and it will continue on all the while the money supply is continually inflated. The economy will be more and more tenuous until it finally fails as market forces overwhelm manipulation and all the malinvestment is purged. The longer it takes the worse it will be. We have the mother of all busts approaching and it is closer than it was yesterday. Be prepared and own solid assets. Gold and Silver is the only real money. The rest will… Read more »

“One of the traditional roles a bank must play in an economy is that it must recycle money from savers to borrowers.” But they have not done this for hundreds of years. A depsit received whether form a saver or a central bank is used as a reserve in the fractional reserve system. Banks lend out multiples 10 times, 20 times even 50 times the amount of their reserve. The money loaned does not exist until the act of borrowing it. Why do you perpetuate the myth that banks facilitate a loan from a saver’s savings? This is a dangerous… Read more »

Monthly Payroll Gains Overstated by 200,000-Plus Jobs

– Contrary to Common Experience, May Payrolls Purportedly Regained Pre-Recession High

– May Unemployment: 6.3% (U.3), 12.2% (U.6), 23.2% (ShadowStats)

– Year-to-Year M3 Growth Jumped to 4.6% in May

– John Williams, Shadowstats.com, June 6, 2014

—————————————————————-

Everything is manipulated to make it look advantageous

“Watching Irish treasury yields fall below those of U.S. treasuries yesterday puts a decided exclamation point on the aforementioned global expectation of “QE to Infinity”; as like the BOJ, the ECB nears the end of its arsenal of money printing schemes.”

Andy Hoffman

http://blog.milesfranklin.com/whatever-it-takes

http://www.youtube.com/watch?v=RcNwt4WgTMg&feature=youtu.be

“This bottleneck chokes off recovery and allows deflation to take hold. Deflation is when prices are falling” No deflation is when the money supply is reduced and the value of the currency rises and so buys more goods. Those things that people need, food , energy, even insurance are increasing in price at a fast rate. 10-20 per cent p.a.Money supply is increasd exponentially the last 5 years. Inflation is in the pie and well and truly baked in. Those things that people want but cannot afford are dropping in price because of lack of demand. It is not deflation… Read more »

A passionate condemnation of the US and the G-7

http://www.paulcraigroberts.org/2014/06/06/lies-grow-audacious-paul-craig-roberts/

“The ECB is deeply Latin now. And it is doing what all Latins do in a crisis: print money” defaming the “Latins” is patently rediculous. The biggest money printers on the planet are the anglos. US and UK. Now followed by the Japanese, europeans and even the chinese. Every Central Banker prints and it is a central banker edict to do so. We are going down the tube with competitive devaluations of currency. A race to the bottom as forcast years ago by some on this very blog!! ALL central bankers think this way. They are trained to break the… Read more »

Nigel Farage is of the opinion that the UK will leave the EU and after it does Ireland will follow to its natural resting place namely an independent Sterling

You only need to compare the weekend’s saturated media coverage of Draghi’s storm-in-a-teacup announcement and the three year media blackout of the escalating Fukishima nuclear disaster to know we are indeed living in a freak show. How any sensible person can comment on present global economics without reference to the deteriorating Fukishima emergency is beyond insult. (ps I refer to all media punditry) Future history books will have a chapter “2010-2020: Fukishima Fallout on the Northern Hemisphere”, while our economic woes will be relegated to a side note, if at all. George Carlin is laughing heartily in his grave. Complete… Read more »

Printing money to excess is the preserve of the central bank in supplying reserves and the chartered bank using the reserve in the fractional banking scheme to produce 10-50 times that reserve amount. The same scheme s used in all manner of places where the paper promises far out weigh the ability to deliver on that promise. In china it was recently reported that physical copper has been sold many times over with paper promises and that hundreds of thousands of tonnes of copper is missing. The same is true for gold bullion on the LME where it is acknowledged… Read more »

http://blog.milesfranklin.com/and-its-gone

Here is a very intelligent view of the ECB’s actions. Makes a lot of sense to me.

http://www.zerohedge.com/news/2014-06-10/alasdair-macleod-all-you-need-know-about-negative-interest-rates

I disagree. I completely disagree. The premise that inflation is the solution does not add up. Inflationary policy, via low interest rates under Trichet fed the asset booms in the PIGIS on the periphery, ten years ago. Japan is now printing money, and it is a mess. Zimbabwe tried it. Argentina tried it – about a dozen times. How, Mario the muppet wants to do the same again. The current ECB interest rate policy is absolutely bonkers. It prevents liquidations of investments. But, liquidations are the only solution. Japan failed because Japan avoided liquidations. Debt is holding the system back.… Read more »

If only the Roman Empire tried inflation……

Maybe if they tried inflation, and invading the east……

[ If this re-balances Irish bank lending away from property into start-ups and companies which produce things, it could be a huge positive for an economy like ours that has a weakness for destroying itself with its property obsession. ] David – the same idiots are still in charge. Just look at the “Irish” banks. Or the big players in Dublin business. 98% of the people in the regulatory authorities are still in the job. Intellectually, there has been no progress. The same morons are in charge. They got burned. But it would be too much to expect that they… Read more »

Tony, I don’t know if it was your intention but you described perfectly what a crazy pipe dream leaving the Euro would be. It is pure fantasy as you explained so well above and I am surprised at Adelaide sharing such a view without explaining where Ireland would go currency-wise. Of course David McWilliams can be pardoned for openly advocating exiting the Euro because he is essentially a Unionist and believes we should rejoin the British Pound and eventually the United Kingdom. He keeps reminding us that the UK is our biggest trading partner, but like Adelaide without explaining why… Read more »

Tony, my main reason for supporting Ireland in the Euro is based on my understanding of what happen to the Asian Tiger economies during the 1997 Asian Financial Crisis. http://en.wikipedia.org/wiki/1997_Asian_financial_crisis. If those independent Asian countries had a common currency like the Euro they would not have been ruined by what amounted to a bank run by hot international investment money. To me the lesson is: if George Soros can “short” the Bank of England (which he did and made his first billion) he can manipulate any currency for a quick profit. So can others. Soros has admitted to having shorted… Read more »