The frenzy has started again. Six years after a property boom practically destroyed our economy, we are at the same nonsense again. When are we ever going to learn that buying and selling over-priced houses to each other is not going to make us rich, but will make us poor?

At the moment, there is no credit in the system and no leverage, but this won’t last. Credit will find its way back into the Irish property market in time and then we will, yet again, take our seats in the rollercoaster, with predictable results.

All week, I have been subjected to relentless propaganda by the usual coterie of property pornographers suggesting that the frenzy is normal. It is not. No other European country destroys itself with such regularity, bar the British – and even they don’t do it like we do.

Today’s mania has been fuelled by two myths. The first is that there are loads of young people looking to buy homes in Dublin now. The second is that the young population is growing.

We are told there is a massive demographic bulge emerging of young people, particularly in Dublin, who needs thousands of new houses and apartments. This contention is taken as gospel and repeated by newsreaders and producers of radio shows and in no time people are queuing up to buy houses – this time with Mummy’s and Daddy’s money.

Well, can I tell you something?

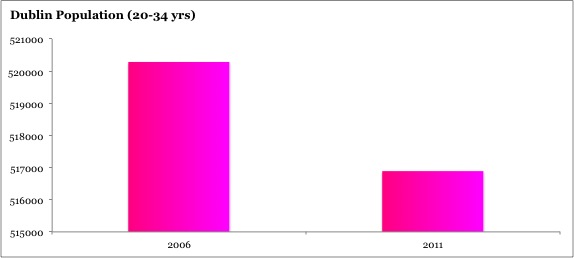

The population of the crucial demographic between 19-34 actually fell in the last census. Not only is the population not rising, it is falling in the capital. Look at chart one. This shows you the change in the population in Dublin between 2006 and 2011 of the critical age cohort 19-34. In 2006, it was 521,000 and more importantly it had been rising very rapidly. These were the Pope’s Children cohort, a reflection of the baby boom of the late 1970s and early 1980s.

Now look at the figure for 2011. The population in the city of 19-34 year olds has actually fallen by 5,000, not by much, but it has fallen. Where have they gone? Many have emigrated and also there was a dramatic slowing of the baby boom by the later 1980s – itself, a function of the 1980s emigration surge in people in their 20s.

So myth number one is not true. The population of ”twentysomethings in Dublin is not growing, but it is actually falling or at best it is static.

The second myth is a more general yarn, which contends that Ireland has a massively young population coming up behind us that will need lots of houses and apartments in the next few years when they move out of home.

This is also not true. Have a look at chart two. It shows you the Irish population pyramid and it reveals what anyone who has been looking at birth rates could have told you. There is a dramatic fall-off in the population of teenagers and early twentysomethings in Ireland.

Look at the pyramid. You see the population bulge in 2011 was in the 30 to 34 age group. These people are now heading towards 35 now on average. Behind them, the population falls off quite sharply. So, for example, there were 420,000 people aged between 30-34 in 2011, but only 300,000 odd between the ages of 15 and 19. This is a difference of 120,000 and this is a substantial figure in the context of the housing myths.

Adventurous people

The reason it is substantial is because these people who were between 15 and 19 three years ago are not between 18 and 22. This is the time the more adventurous people begin to move out. In time most, but not all, of them do. A few years later and they will begin living with their girlfriends or boyfriends and they will begin to nest.

Nesting drives the economy because people tend to buy stuff they had when they lived at home. So rather than one kettle there will be two, and two sofas and beds and fridges. The parents keep their room, with the bed made, but they have moved out and are buying stuff for themselves. This ”nesting is what drives consumption of ”big-ticket items, queues at the check out at Ikea and retail sales all over the developed world. It is also what crucially drives house buying.

So the demographics are telling us that we will have as many as 120,000 fewer people moving out of home and looking for a place to live in the next few years than we had in the first years of the century. This is a huge issue for a housing market whose pornographers are painting a picture of hundreds of thousands of new twentysomethings hanging out in town, looking for place to live and party.

The truth is that there will be far fewer of these types of Irish people out there then there were ten years ago. So unless we are going to see a policy of forced repatriation of over 100,000 people aged 20 to 25, where is the demand for housing going to come from?

This leads me to what is happening now because the price rises in Dublin and other urban centres are real. Indeed, despite the analysis of demographics, I think house prices will continue to rise because what is happening this is a form of savings or pension fund provisions for rich middle-aged people.

The cash buyer is the buy-to-let player of a few years, except he is doing the buying without a mortgage. He is taking his wealth out of the banks because the banks are yielding nothing on his savings and he is buying a house, playing the capital appreciation game, paid for by the renter who is priced out of the market by the guy who ends up being his landlord.

On Thursday, the ECB softened up the ground for zero interest rates in Europe. This will drive more money out of deposits. This could ironically cause mortgage rates to rise (not fall) in Ireland as the still bust banks try to make money on lending.

This process will drive an even bigger financial wedge between the first-time buyer and the old cash buyer, exacerbating the sense of a housing crisis, when there needn’t be a crisis at all.

Ultimately, in an environment of zero eurozone rates, new credit will come in as it always does and we will be off again into bubble territory. Except this time we won’t even have the demographics to support it.

We’ve been here before. We know how this story ends.

David McWilliams writes daily on international economics and finance at www.globalmacro360.com

Subscribe.

David,

How do you make the assertion that bank lending for mortgages will increase? QE? In the US, we had massive QE programs but the money didn’t flow to Main St.

Also, prices have begun to fall in Dublin (according to the CSO), granted only for two months, but FTB’s are getting priced out and perhaps we have some ‘cash buyer exhaustion’ – we could be looking at the end of the echo bubble in Dublin already.

Moon Wobble

Tomorrow ………..is the 7th Day before the ….Moon Wobble…Full Moon ….Blood Moon ….and …Feast of the Passover …..and all of this Peaks ….on the 15th April .

Remember last months 7th Day warning ….the Flight Plane disappeared and still has not been found…..and its flight number was 370 .

GO SLOW ……VERY SLOW…..and….STOP

Good article David. If the government (and main stream media) were to look at Maslow’s hierarchy of needs they would see that our most basic human requirements are Food, Water, Shelter and Warmth. Government policy is ostensibly focused on keeping Food, Warmth (energy) cheap and, until recently, Water free. They would not countenance, nor would the media, the idea of people profiteering on such a fundamental human right as water. Nobody would cheerlead some guy who bought 10,000 gallon of water just to sell it on to someone in need at a massive profit. Yet such people were the poster… Read more »

It’s not speculation that’s the only driver – at the end of the day it’s basic supply & demand of a scarce resource economics. It was always the availability of finance that drove the market – this time around there’s restricted supply in the areas that people want to buy. The lead-in time for new demand is very slow – the only question is whether or not this is a mini bubble or a sustained increase…

Hi David, Great article, but you forgot to mention the government/bank policy of Socialism for the rich, which means those living in South Dublin who no longer pay the mortgage are being allowed to stay in-situ, without any threat of re-possession, which lowers supply to the market, which puts up prices. Hats off to Adelaide here a few weeks ago for a great post. *** ——- ****** Adelaide March 4, 2014 at 10:12 pm Hi Tony Talking of manipulated data there was an economist earlier on the radio discrediting today’s press release “Central Bank shows 3.3% decrease in mortgage arrears”… Read more »

Looking at that population pyramid, it screams “No State Pension for Me!!”.

I’m 47 years old. If I retire at 67, I’ll be depending on middle-aged working people to pay my state pension – and there obviously isn’t going to be enough of them to support all us oldies.

Napoleon recognised the needs of his wounded and sick soldiers after war and when they returned home to France with nothing . He knew that they could not get a bank loan or have funds to purchase a house and that they wanted to live in the place of their childhood dreams . He acknowledge all of that yet he wanted to reward them and this was another challenge for Napoleon on his home turf .To show that he remained a true leader acted on the Codes he had being building up all along and devised a new concept —… Read more »

Thanks to all for great comments and David’s article.

Up till now the trend was that the children leave the nest and buy their own house including all the bits and pieces for the house. Most parents help their children in getting their own household up and running by helping out with a fridge, washing machine and other smaller investments.. The parents then remain in the family home which, most likely fit a big family comfortably anyway while the children buy smaller starters home. These parents are also most likely mortgage free and not spending any more money except on their “independent” children. Other than that these parents with… Read more »

Hmmm, great article, thought provoking but as to its consclusions not at all sure: Why? 1. Whilst the population in the 20-34 cohort are not growing as quickly as before there are still more of them coming on stream than appear to be leaving the housing market, so yes a lower rate of growth, but net growth is still surely a net driver of housing demand and hence prices (subject to supply,etc) 2. the 20-25 and 25-30 cohorts are significantly lower than previous due to emigration in the last few horror years, but with a growing workforce at the moment,… Read more »

That article has “wake up call” embedded in it. The one dynamic that is outside of the article is the “tech sector” boom in Dublin. Compare Dublin to Waterford, Drogheda, Dundalk or Navan and you get an insight into the role of tech in the Irish housing market. Medium sized population centres are not moving anywhere, in terms of real estate valuation. That is the real state of the Irish economy. There are two factors influencing incomes in Dublin that are based on capital inflows that are not sustainable. 1. State borrowing. Very few quangos outside of Dublin paying Angela… Read more »

At some point in time the entire SCD real estate thing will fizzle out, and be seen for the nonsense that it is. It is not Southern California or Florida. The weather is better in Wexford, and in winter time along most of the south coast. It is purely a variation of status obsession. It reveals deep psychological obsessions, and needs. In Ireland, there is a deep connection between real estate and status, and the right to feel good about oneself. It goes back to the “good room theory”. And an obsession with external status, even to the point that… Read more »

David,

Full Reserve Banking and Land Value Tax reforms would probably fix this problem.

http://neweconomics.net.nz/index.php/2012/05/land-and-money-the-siamese-twins/

Kevin

“This leads me to what is happening now because the price rises in Dublin and other urban centres are real” So much for the nonsense about deflation because rents are skyrocketing also. “When are we ever going to learn that buying and selling over-priced houses to each other is not going to make us rich, but will make us poor” You miss the point there. Further down the article you identify cash buyers as the culprits for driving prices. Probably correct. You suggest that they are in it for the capital gain. Maybe not. Maybe we are back in the… Read more »

Declining Population: I was working in the border counties post-Christmas Louth-Monaghan-Cavan, and it was sad and a genuine shock to return to towns I’m fond to see them in such miserable state. Talking to locals, the cause is the birth rate. The border counties were always employment black-spots and emigration was always high so nothing has changed in an economic sense to explain the demise of these towns. What has changed is the end of the ‘big family’. No more 6-9 children families. The locals would describe family cars brimmed to the full of kids spilling out for Sunday mass.… Read more »

At Peter Ustinov put it, an economy based on everyone doing each other’s laundry, at ever increasing prices.

Good article David, and you’ve picked up a lot of truths. What I have noticed, for reasons I can’t share, is that there is a huge bulge in arrears and reposession activity happening at the moment, especially with the smaller banks. The forebearance policy has given in to “get the money in now.” A huge new arrears dept is opening in one of the pillar banks. Another one of the smaller players currently has a very busy arrears department. The pressure is not on anymore to get full payment but to get ANY payment. Agents are phoning up cold looking… Read more »

0% Interest? Free money then? Are ‘banks’ even offering long term saver account deals anymore? Where you agree that you will get a higher interest return so long as you do not withdraw amd continually deposit a minimum amount for X years?

Basically can we not have a 2/3 or 4 tierd interest concoction so we all get what we want-Too much to hope for?

There are no unmanipulated markets.All is distorted including interest rates, (housing markets) (Bond pricing) stock markets and all things financial. got to be rid of the system or all this debate on local topics is a waste of time. From Lemetropolecafe.com It’s rainy and cold this April spring afternoon in Dallas, an area that has become weather jinxed when hosting very visible major sporting events. Three years ago it was the Super Bowl in Arlington, TX, which is right next to Dallas. The snow and ice leading up to the event was so bad it made travel to any scheduled… Read more »

Economists are largely bought and paid for. “I have seen the enemy and it is us” (them)

http://henrymakow.com/2014/04/Economists-Sell-their-Souls-to-the-Fed.html

Turk: “There are so many economic distortions throughout the world today, Eric, no wonder so many people are totally confused about what to do with their money. The central planners are hard at work pursuing policies that are destructive to markets. They do not understand or are completely oblivious to the fact that their constant interventions are perverting economy activity….

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/4/7_Record-Breaking_Gold_Backwardation_Shocking_Banks_%26_Shorts.html

so when is the acknowledgement of the fixed markets, the fraud and deception, to be discussed , David. when are you going to start educating the people?

“Today a man who has been involved in the financial markets for 50 years warned King World News about a horrifying situation for the West that will also bring the United States to its knees. He also warned the artificial control of markets will end in disaster. Below is what John Embry had to say.”

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/4/7_This_Is_Horrifying_For_The_West_%26_Will_Bring_The_US_To_Its_Knees.html

How about an essay on the Presidents working group on financial Markets. AKA the plunge protection team.

The housing market and the low interest rate phenomenon is not a local, ut an international problem. Running to australia or Canada is no solution. The monetary system needs changing and to start Ireland should take note of Russia and use its own debt free treasury issued money. From David Schectman. Jim Willie is one of the most original thinkers in our industry. His newsletters are long and not for the average casual reader, but here are some of his most recent thoughts via an interview with Greg Hunter at USAWatchdog. Whole Eastern World Rebelling Against the Dollar-Jim Willie –… Read more »

The trouble is the lousy stinking money system we have. Comments by Jason Hommel Here are some thoughts that came to me this week. I shared them on facebook a few days later. It was one of my most popular recent posts. https://www.facebook.com/jason.hommel Silver is money, rare, honest, true, heavy, measureable, weighable, countable, the best electrical conductor, a great heat conductor, the most reflective metal, good, pure, shiny, acoustical, antibacterial, valuable, the free markets choice for thousands of years, rewards production, savers, and thrift, maintains honest and limited government, restrains government, promotes freedom, is slandered, misunderstood, ignored, undervalued, overlooked, maligned,… Read more »

Noonan’s comments on the housing market, are bad timing. Nasdaq dropping. Tech sector in trouble. Revenue is not sustaining the captal investment – instead it is being sustained by dubious “investment models based on social media companies and internet 2.0 stocks (“the cloud”). It has all the classic signs of an investment bublble. Tulip mania, SouthSea bubble, etc….The “projections” are not going to turn into cash flow. And for anybody living outside of the DART line area of Dublin and NE Wicklow the comments are slightly inappropriate. What happens to the Dublin real estate market when the capital inflows resulting… Read more »

Economic Reality versus Illusion:

* Economic Reality versus Illusion: No Recovery, Just Plunge, Stagnation and Renewed Plunge

* Re-Intensifying Downturn Already Underway

* Confluence of Negative Surprises, Including New Business and Systemic Woes, Should Hit U.S. Dollar and Spike Inflation

* Hyperinflation to Intensify Unfolding Depression

* Gold as a Store-of-Wealth and Safe-Haven Remains Primary Hedge for Maintaining Purchasing Power of Wealth and Assets

-John Williams, Shadowstats.com, April 8, 2014

Are we going to have a real shooting war with russia to divert the 100 million unemployed and the 50 million on food stamps.?

Russia putting the finger to Uncle Sam ?

http://usawatchdog.com/weekly-news-wrap-up-4-11-14/

Nama should turn its properties into affordable housing and some social housing following the example of Singapore. There is global savings glut, with the aging population and pensions a part of that, also Sovereign wealth funds and oil backed funds. The printing of money in the US, Japan and the UK etc has added to the cash floating around. This money is looking for a return and its not getting it in bonds. Rental income Property, both residential and commercial is seen as a long term safe type investment. As the Irish economy picks up this money will find its… Read more »

Good article and would agree with summation that the current bounce (dead-cat) is stemming from two things, cash rich “investors” with a lack of available alternatives whose average age profile is of an older bracket and therefore more risk averse, thus by default look to an area of investment that they “know” something about, first off an EU1.5mln family home in SoCo Dublin that is now say eu750-eu800k appears to be great value to many regardless of whether it should have been “worth” eu1.5mln ever the same way that im sure dutch tulips found buyers on the way down also.… Read more »

[…] PRICE is NOT "CHEAP". No Doubt you'll condemn this source, just like Bertie. No country for young buyers | David McWilliams The frenzy has started again. Six years after a property boom practically destroyed our […]

[…] of thousands of new twentysomethings hanging out in town, looking for place to live and party. No country for young buyers | David McWilliams I knew you were a saddo from your first post- now go get that life Sign in or […]