Here is an extract from today’s Global Macro 360 Daily Note. To read the full content click here to sign up for a One Week Free Trial.

Summary

- Jittery Markets: We are trading away in this volatility

- United Kingdom: The UK is flying, rates to move sooner not later.

- Russia: Not cheap enough to buy yet.

- United States: Trade balance improves, but $ moribund

- Australia: Wobbly Wallabies

- Eurozone: German factory orders slump

Good morning,

Everyone is now officially freaked out about Ukraine which we have taken as a signal to trade jittery markets a bit more actively and we will tell you about these moves in this morning’s note.

European equities are weaker again this morning. Yesterday only Oil & Gas were up +0.17%, but all other SPX sectors are in the red. The DOW closed down 129 to 16401 (-0.78%). SPX closed down 17 to 1867 (-0.90%). NASDAQ down 57 to 4080 (-1.38%). We took profits on our long US equity market volatility position and we intend to buy back on any dip in coming days.

The USD was also weak across the board and the Aussie dollar was the main outperformer, up +0.85% after the RBA rate decision was unchanged. The EURO also traded stronger after industrial confidence bounced in Spain and Italy. We reacted to yesterday’s move to add to our Euro position ahead of the ECB tomorrow. Sterling also rallied to $ 1.7000

Speaking of Sterling, let’s start today in the UK, where things are looking up yet again.

United Kingdom: Business sentiment improves in April

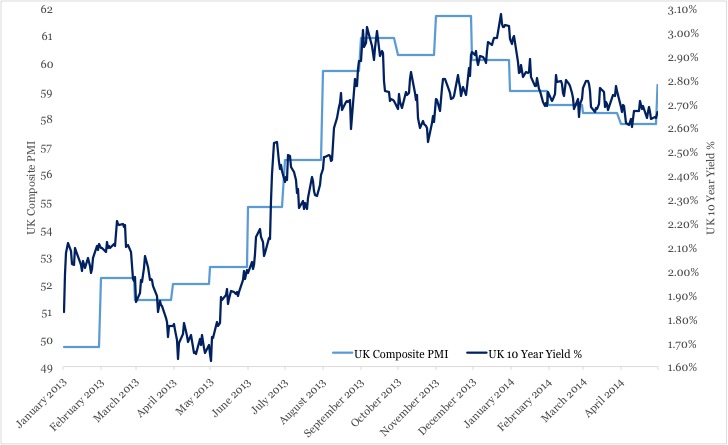

The UK services sector PMI rose from 57.6 to 58.7 in April, a larger rise than was expected (Cons: 57.8). With all the data now in for the total PMI, we see that confidence in the UK is still on the up having moved from 57.2 to 58.3. Such levels of confidence are consistent with a bumper +4.9% annualised growth in April – by far the most stellar performer of the developed world economies.

The UK services sector PMI rose from 57.6 to 58.7 in April, a larger rise than was expected (Cons: 57.8). With all the data now in for the total PMI, we see that confidence in the UK is still on the up having moved from 57.2 to 58.3. Such levels of confidence are consistent with a bumper +4.9% annualised growth in April – by far the most stellar performer of the developed world economies.

Yesterday’s move higher in the PMI would suggest an increase in UK 10 year yields from here.

Figure 1: United Kingdom Services vs UK 10 Year Gilt %

We believe there will be a move by the Bank of England ahead of most economic forecasters, late this year versus mid next year.

We believe there will be a move by the Bank of England ahead of most economic forecasters, late this year versus mid next year.

To Read more of today’s Daily Note, head over to globalmacro360.com and sign up for a One Week Free Trial . Not only will you be able to read future notes for the next 7 days but you will have access to all content on the Global Macro 360 site.