Here is an extract from today’s Global Macro 360 Daily Note. To read the full content click here to sign up for a One Week Free Trial.

Summary

- Europe: Try getting a job over here!

- Ukraine: Goading the bear

- Equities & Bonds on different trajectories

- United Kingdom: Weakness in mortgages but still bubble territory

- United States: Yanks spending more than they are saving

Good morning

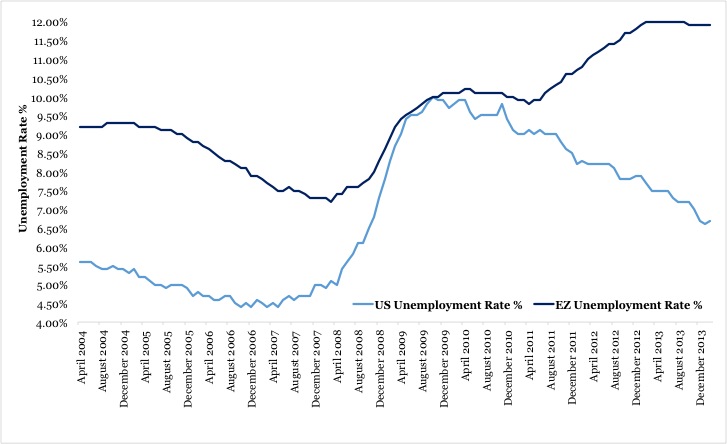

Hope you are in good form this morning as we, at least here in Dublin, head into a bank holiday weekend. Before I talk about geo-political events in Russia, have a look at this chart ahead of today’s unemployment numbers in the US and the Eurozone.

The chart shows you the rate of unemployment in the US versus the rate of unemployment in the Eurozone. If anything explains what is happening in the world’s two biggest and richest economic zones, it is this.

At the end of 2009, both the US and the EU had the same rate of unemployment. Since then, it has become easier to get a job in the US whereas, the opposite has been the case in Europe.

Today, Europe’s unemployment rate is twice that of the US. Enough said. If you want to know why, on a medium term basis, the Euro is way overvalued, just look at this chart.

Figure 1: Giz a job US versus European unemployment rate

Ukraine: Goading the bear

When the interior minister of a former Soviet republic articulates military policy through Facebook updates, you know we have come a long way since the days of Interfax and Pravda.

However, while the mode of communications may have changed, the “might is right” dictum still holds in the region. The Ukrainians have decided this morning to test Putin’s resolve. They are in a difficult position. Up to now, they faced a dilemma: if Kiev does nothing, they will lose eastern Ukraine to the rabble; but if they do something and push it too much, Putin may invade and they lose eastern Ukraine to the Russians. But there may be a third option in play which is to inject an element of doubt into Putin’s mind: by going for a quick military strike in the east, they could wait and see if Putin blinks first.

Putin knows an invasion of Ukraine changes the game dramatically and he may not be willing to throw the dice. If he backs down, he is wounded badly, but if he goes for it, he may be hurt via the impact on the economy of massive capital flight.

This morning we are in a new phase because the Ukrainians have gone in with force aiming to retake government buildings and restore law and order to Slovyansk.

Equities & Bonds see the world very differently

Just before all this, equities ended last night in the US slightly lower after the S&P made an attempt at 1890.

For the third month in a row we are heading into NFP with the equity market at elevated levels. The last two times the market sold off, it took a month to recover; will this month be different?

The consensus figure for today’s employment report is for 230-240,000 jobs to have been created in the US in April.

The treasury market is more cautious than its stock market cousin.

If you consider the chart below, which shows the US 10 Year yield vs US Economic Surprise Index, you can see that the poor US GDP number from earlier in the week is weighing fixed income yields.

To Read more of today’s Daily Note, head over to globalmacro360.com and sign up for a One Week Free Trial . Not only will you be able to read future notes for the next 7 days but you will have access to all content on the Global Macro 360 site.