While you may have been watching the opening game of the World Cup on Thursday night, the Bank of England Governor, Mark Carney sent sterling surging towards a five-year high with his speech at the Mansion House in London.

This move in Britain could have a significantly positive effect on the prospects of the Irish economy.

In the real world of commerce, we have always depended more on Birmingham than Berlin.

As this column has written over the years, Ireland is tethered to the most incomprehensible exchange rate policy because we are use the euro – which is in effect Germany’s currency – yet we do far more trade with Britain.

More importantly, the stuff we sell to Britain, unlike the stuff the multinationals that are based here sell (or pretend to sell, according to the EU Commission), we actually own. These are Irish real goods, made by Irish people, owned by Irish people.

So when Britain is booming, it is good for the Irish economy in a much more amplified way than when other trading partners are booming.

In addition, because Irish people emigrate to Clapham rather than Cologne, when Britain is doing well, there are job opportunities for Irish individuals in Britain which Irish people fill. In contrast, job opportunities in Cologne, are rarely filled by Irish emigrants.

So at an individual level, if Ireland is not doing well, it is better for us that Britain is prospering than if Germany is prospering.

In fact, we can go one further and argue that Ireland’s economic stance in counterintuitive.

For example, the best situation for us is one where Germany and the euro are in trouble, like now with deflation, and Britain is booming.

This oddity is because when the eurozone is in trouble, our interest rates are low, easing the debt burden on hundreds of thousands of Irish households. If sterling is also likely to be strong during these periods, Irish exports to Britain more competitive. So it’s a double positive.

We are experiencing this virtuous combination at the moment.

This week, I am going to use three charts that explain what is going on and how it affects Irish exporters and Ireland.

On Thursday evening, a surprisingly hawkish Governor of the Bank of England, said that Britain would probably have to increase interest rates sooner than later because of the booming housing market. Immediately, sterling surged to $1.6987 against the US dollar and more importantly for us, it reached an 18-month high against the euro. The euro fell to 79.9p.

Look at figure 1. It shows what is happening.

Figure 1: Euro/GBP FX

The euro has been gradually falling against sterling since early 2009 when it spiked up to nearly parity – at a time in Ireland when our domestic economy collapsed.

Due to our commitment to follow Germany, Irish firms saw their domestic market evaporate in 2009 and our currency appreciate (not depreciate) against our biggest trading partner.

It is amazing that anyone survived that negative double-whammy!

Now as you can see, sterling is strengthening and in the chart you can see the euro falling. This is good news for our exporters.

But will it last?

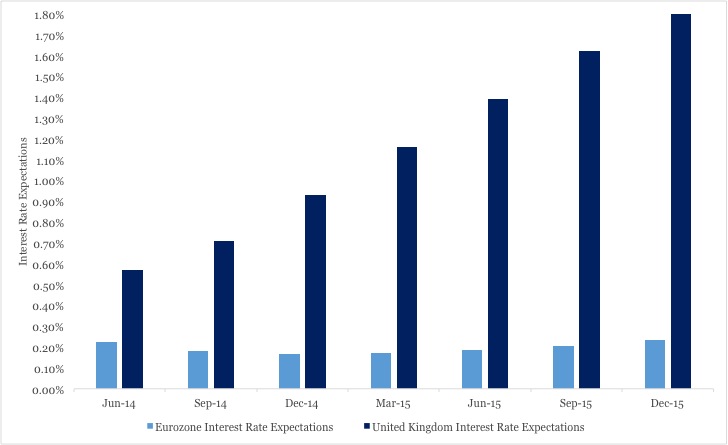

By saying that a hike in interest rates “could happen sooner than the market expects” Mark Carney changed the game and people now think British interest rates will rise faster than previously thought. This should keep sterling strong.

His words also have another psychological effect.

They signal that the world of permanently low interest rates of 0.5 per cent cannot last forever. The Bank of England now becomes the first major central bank to announce rate hikes since the financial crisis of 2007-2008. Many expect others to follow suit, such as the US Federal Reserve.

However, the ECB, which is still trying to defeat deflation, will lag behind. This difference in rates, between the Europe and Britain, is expected to increase and further strengthen sterling.

We can see this change in interest rates expectations in figure 2.

Figure 2: UK vs EUR interest rate expectations

What does all this mean for Ireland?

As Britain is our second largest trading partners, comprising roughly 16 per cent of our export market (and these are real things, not Apple’s makey-uppey exports), all this is highly advantageous to Irish exporters.

A while back, the chief executive of the Irish Exporters Association (IEA), John Whelan, admitted “the exchange rate with sterling has been a barrier to Irish export growth in recent years”.

He went on to say that “an ideal exchange rate is about 70p”.

This sentiment was reinforced by chief executive of Bord Bia, John Cotter, who claimed in 2010 that “one of the single biggest factors in the decline has been the depreciation of the sterling against the euro”.

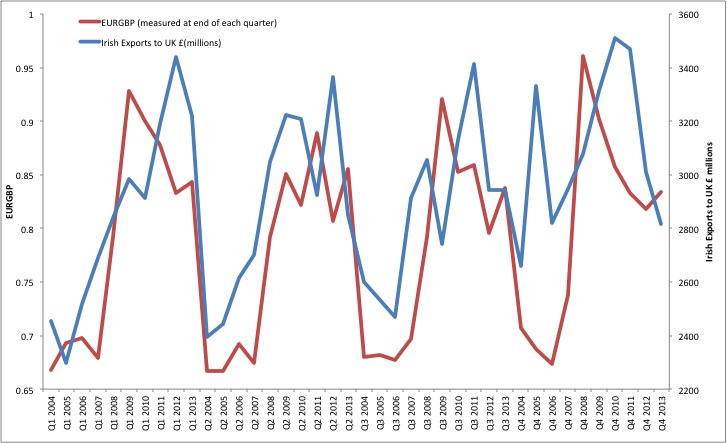

If you doubt this, look at the final chart. It plots the movement of the sterling/euro exchange rate and Irish exports to Britain. You can see that Irish exports, as the head of the exporters claim, are highly sensitive to the exchange rate. A few cent movement in the wrong direction can wipe out the competitive position of many small Irish exporting companies.

Figure 3: EUR/GBP vs Irish Exports to the UK

Quite how any regime could have given away the power over its exchange rate to Europe without much analysis remains one of the most extraordinary moves on the part of Irish establishment.

The exchange rate is crucial. Indeed Paul Volker, the former head of the Federal Reserve described the exchange rate as “the most important price in the economy”, I agree with him.

We know that sterling’s value is of huge importance to us. We are the only euro country with a land-border to the sterling area and we also have what I call the “Sainsbury’s Index” of exchange rates.

The Sainsbury’s index is the most telling indicator of over or undervaluation any exchange rate has. I am talking about Sainsburys in Newry

When the euro is too strong against sterling, the best indicator of this overvaluation isn’t some fancy chart, but is the eight-mile tailback at the roundabout in Newry of people from the Republic stocking up with cheap British booze for the Christmas.

In contrast, when sterling is strong, you’ll see no slabs of cut-price Tennents stacked in the boots of Toyota Corollas in the Sainsbury’s car park.

For the foreseeable future sterling and the British economy will be strong and European interest rates will remain low. This combination is good news for Irish exporters and this should be welcomed.

David Mc Williams hosts a discussion with a panel of experts next Sunday evening on the topic “South Dublin Houses – time to buy or time to sell”? at the Dalkey Book Festival. Tickets at www.dalkeybookfestival.org

Subscribe.

The feel of Sterling in my hands just feels like coming home and connecting with a time that has since eclipsed me.

That Sterling bond is sterling in strength stamped with Royal Approval HRH and does not bend.

My Euro emulates an Italian Carnival Carousal with ringmasters and music and the rest is in my imagination.A paper in name and appearance and a diet that can be consumed by any prey near me.

I am not an economist McWilliams but your view on deflation may not be as clear cut as you think: http://www.ritholtz.com/blog/2012/10/seven-varieties-of-deflation/ Which deflation are you talking about? Some time ago you informed us the housing market in Germany is overheating. This article references the housing market in the UK overheating? The Dublin Housing market is going balubas. Rents sky rocketing. Ditto for London rents. No one I know got a letter in the post saying prices were dropping. The stock markets are making new highs. And all of this where banks are putting money on deposit with to get safe… Read more »

The sterling collapse against the euro went totally unremarked at the time. I totally noticed as an Irishman working in England on what was a salary increase when I moved that within two years I was earning less, in Euro, by far than I had left for. Yet, nobody in the UK or Ireland really commented on it. It was 1.6 euro to the pound. Now its 1.26 and it was near parity at one stage.

“In the real world of commerce, we have always depended more on Birmingham than Berlin.” You’ll get the West Brit brick-bats for this one, David. LOL! There’s a real pain barrier for the Irish Establishment to go through before they are prepared to re-visit the fateful and absurd decisions that led to the Euro and becoming a satrapy without control of interest rates. Birmingham has one of the youngest demographic profile cities in Europe and with the ‘Trojan Horse’ Muslim school stuff and Tony Blair raving about invading Iraq again over Isis: a flash-point scenario for the world’s future. It… Read more »

It is amazing to me that apparently educated Irish readers on this site gobble up this pro-British dribble every day. Today McWilliams writes a whole piece praising the beneficial effects on Irish exports of a strong Sterling without a single word about its devastating effects on Irish imports and Ireland’s cost of living. Ireland is forced to buy all its capital equipment from Britain because when joining Europe it stuck to outdated British standards. The mistake was not in joining the Euro but doing so without joining the rest of the world and leaving behind the old British Empire and… Read more »

I remember being on holiday in Corfu, with my expensively purchased Starling cheques the weeek of the notorious ‘Black Wednesday’…yes to go on holidays from Ireland, you had to buy sterling ! I remember having to buy sterling to import goods to Ireland for re-sale with a different sterling rate for each purchase. Maybe Mr williams doesnt remember the joys of being linked with sterling ?

No thank you…I would rather continue being able to hop on a plane with my own euros and fly to wherever i like in Europe, i.e Euro Europe.

Anglophobia and Anglophilia are the twin curses of Irish political discourse. In an argument over whether we should be tied to sterling or tied to the euro, a proposition that is never put forward is whether we should, for the first time ever, actually have our own currency! Tying our currency to sterling from 1922-1979 was the monetary equivalent of James Connolly’s dictum about painting the red postboxes green……. IN his book, “Sins of the Fathers”, Conor McCabe has some brilliant inisghts into the monetarist headbangers who ran the country from the Dept of Finance, the Irish branch of the… Read more »

The currency issue is only a small part of Ireland’s economic issues. Ireland could switch to its own currency and “serve neither King nor Kaiser” as you put it, but it would still have to buy all its capital and much of its consumer products from Britain, not because of currency issues but because of standards compatibility issues. Everybody here in Ireland seems to accept that they are de facto part of the UK. The world’s suppliers consider it one market. They rarely appoint separate distributers for Ireland. Ireland has virtually no ecommerce of its own. It is a mere… Read more »

Buckets & Spades Why is it so sunny this week .Is it because there are no clouds above us ? It is because the wind did not blow the clouds towards us .It is sunny because there is no wind not because there are no clouds. Why is there a booming Britain ? Sterling and Euros are found in print and in the pc and in a local circulation territories close by .Yet they each have a different value and a varying one .The varying value is what is relevant .The Swing and significant variation is what causes the Boom… Read more »

This article reminds me of a post I made here over 5 years ago where I thought we could take advantage of our position between the Anglo/Americans and Europe. I was more optimistic then as I believed that the people running Ireland were searching for solutions that would serve the common good, a bit like your good self David……..Ah well I might as well dream here as in bed….. jim says Irish economic policy pushed through by the PD/FF administration of the last couple of years has been one of low tax, low wage to productivity, competitive in the sense… Read more »

Who is going to save Ireland? Not the bankers, it seems, so will it be the EU? Booming Britain? Or Booming USA?

I think that this is Pat Flannery’s fundamental point: It’s always about “who’s going to save Ireland?”. Major trading partners are always important, whoever they are, but perhaps there would be more clarity from “How are the Irish going to save Ireland?”. Or are we still thinking that any economic difficulties *must* be someone else’s fault, so someone else must fix it?

There are a few different Irelands. Public Sector Ireland is enjoying the full luxury treatment in their silklined Jobs/indexed pensions for life and many PS retirees are clients of the wealth management depts of accountancy firms who are advising them on how to invest their huge retirement lump sums…no I am not joking..ask any accountant involved in this sector. Some are eyeing up opportunities to re-enter the property market. Many in the private sector professional area are doing very well whilst some from that sector are unemployed. People like Mr Williams himself are we assume also doing very nicely thank… Read more »

Our “exports” that make it in Britain are not exactly high margin exports. But they are exports that are very good at providing employment. Because the traditioanl export sector to Britain existed on the basis of previous competitive strengths, including labour cost. At this point in time we have lost the labour cost competitiveness. The entire sage, of Ireland’s public policy, nonsense from IBEC and ICTU, the obsessive pursuit of “inward investment” via low taxation rates for corporates, and the mad consumerism that the gombeen element in Irish politics (and the media) is trying to get drive upwards, is that… Read more »

Britain and debt.

Neither Mark Carney, nor David Cameron, David McWilliams has dared to mention the elephant in the room that is the British economy.

It seriously undermines Britain’s long term financial viability.

The topic of debt is top of the list of controversial topics, about which there is no more honesty in the debate in Ireland.

[ A while back, the chief executive of the Irish Exporters Association (IEA), John Whelan, admitted “the exchange rate with sterling has been a barrier to Irish export growth in recent years”. ] And therein lies an indication of Ireland’s “competetiveness” versus Britain. The Irish exporters lobby group says that everything depends on the exchange rate. They capital is not available to invest in the reduction of unit costs, or other technical innovations to retain market share. The capital is squandered. Very little gets accumulated anyway, due to the Irish cost structure. Just look at the cost of operating a… Read more »

[…] > Read more […]

People, probably by far the majority, who accepted and believed that markets were free and without officially condoned intervention and manipulation have suddenly acquired new headwear with the publication by the Financial Times thatcentral banks own almost 50% of the stock traded on global stock markets! In terms of the numbers involved, we should perhaps now refer to the “Tinfoil Helmet Army Group” – it is no longer a mere Brigade who live the life of make believe!

Regards

daan

Posted in lemetropoleCafe. The stock markets are so manipulated they bare little relationship to reality.

Fantasy is beginning to fall to reality

http://voiceofrussia.com/2014_06_18/Putins-aide-proposes-anti-dollar-alliance-to-force-US-to-end-Ukraines-civil-war-8030/

The Blog of My Life

I think having read Deco recent very readable contributions it should be fitting that our host should write a new book with the significant contributors to this site over the years .It would be a fascinating book .I have no doubt it would be a best seller and record in history .

[…] Bank on booming Britain – Click on David’s name to get back to the home page at any time. These icons link to the main sections of the site, and you’ll find them in the same position on every page. The Writing section contains articles, and information about David’s books … […]